PPT Chapter 23 Statement of Cash Flows PowerPoint Presentation, free download ID9244480

Problem 16. Each of the following items must be considered in preparing a statement of cash flows for Blackwell Inc. for the year ended December 31, 2010. State where each item is to be shown in the statement, if at all. (a) Plant assets that had cost 18,0006 dollars \% years before and were being depreciated on a straight-line basis over 10.

Components of the Cash Flow Statement and Example

Chapter 23- Statement of Cash Flows. 34 terms. jessica_gormley. Preview. Cash Flow Statement. 36 terms. PhelpsPhan1. Preview. BA 530 - Financial Management (Charles Hodges) - MidTerm. 21 terms. Taylor_Hartke4. Preview. chapter 6 Income statement. 55 terms. quizlette3156855. Preview. ISOM351 Final Exam Review.

Chapter 23 Statement of Cash Flows

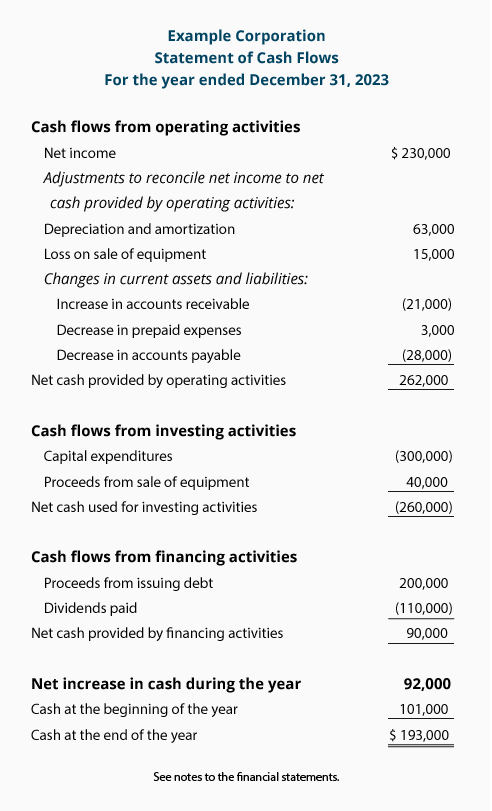

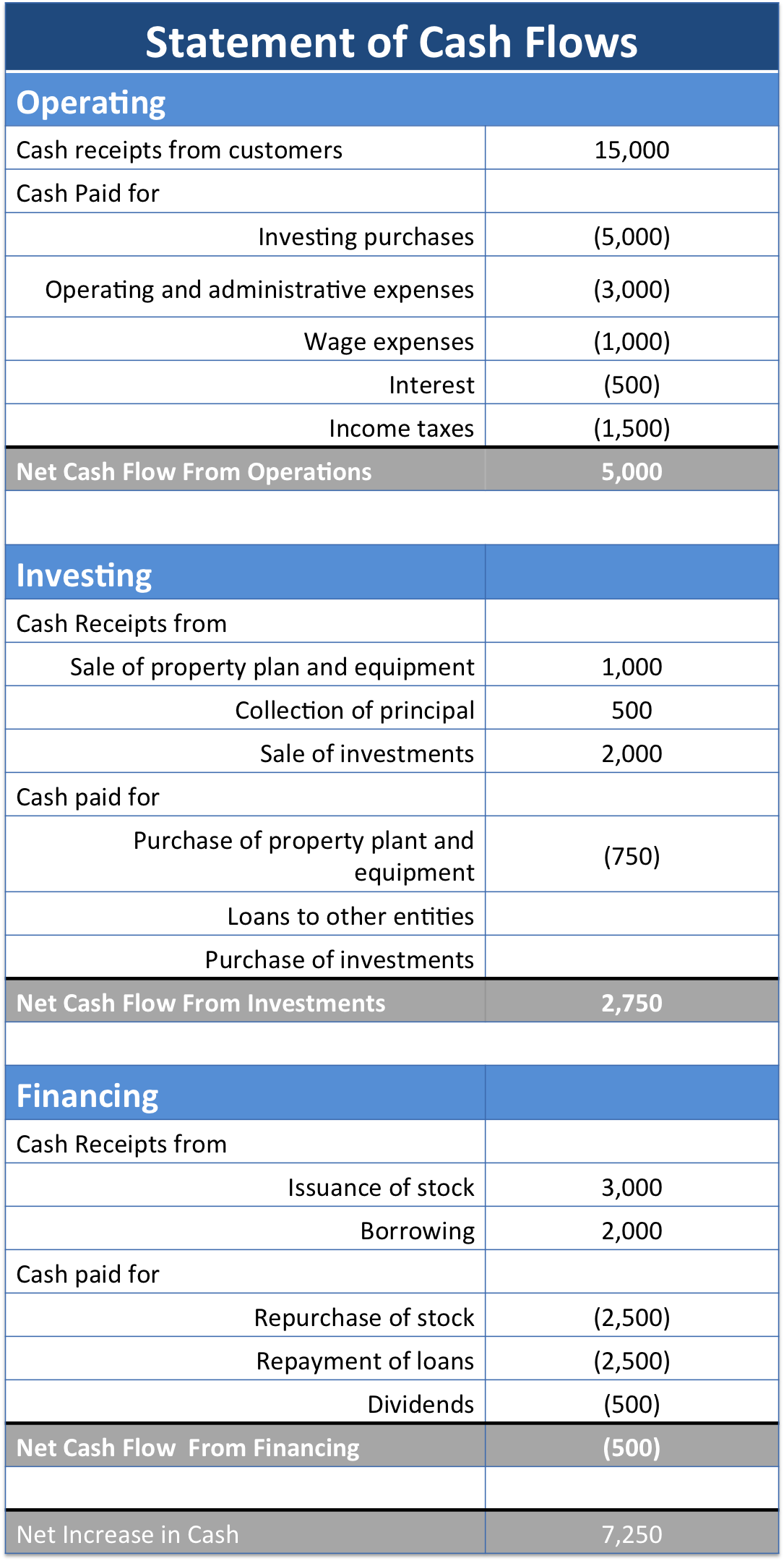

A cash flow statement is a financial statement that shows the cash going in and out of a business over a set period. A company's accounting department keeps track of every transaction that involves cash, such as receiving money when a client pays an invoice or sending money out to make payroll or meet a loan payment.

Statement of Cash Flows Template, Calculation, Methods, Example

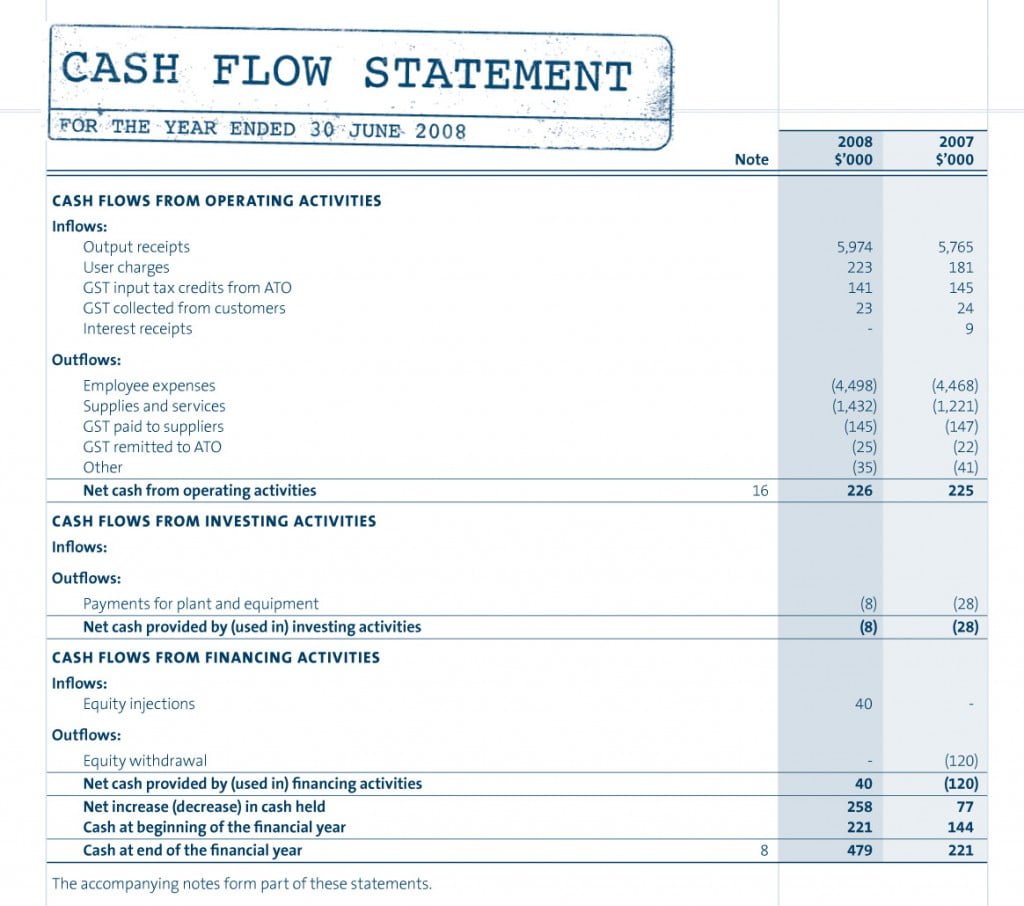

IAS 7 Statement of Cash Flows In April 2001 the International Accounting Standards Board adopted IAS 7 Cash Flow Statements, which had originally been issued by the International Accounting Standards Committee in December 1992. IAS 7 Cash Flow Statements replaced IAS 7 Statement of Changes in Financial Position (issued in October 1977). As a result of the changes in terminology used throughout.

Cash Flow Statement Explanation and Examples AccountingCoach

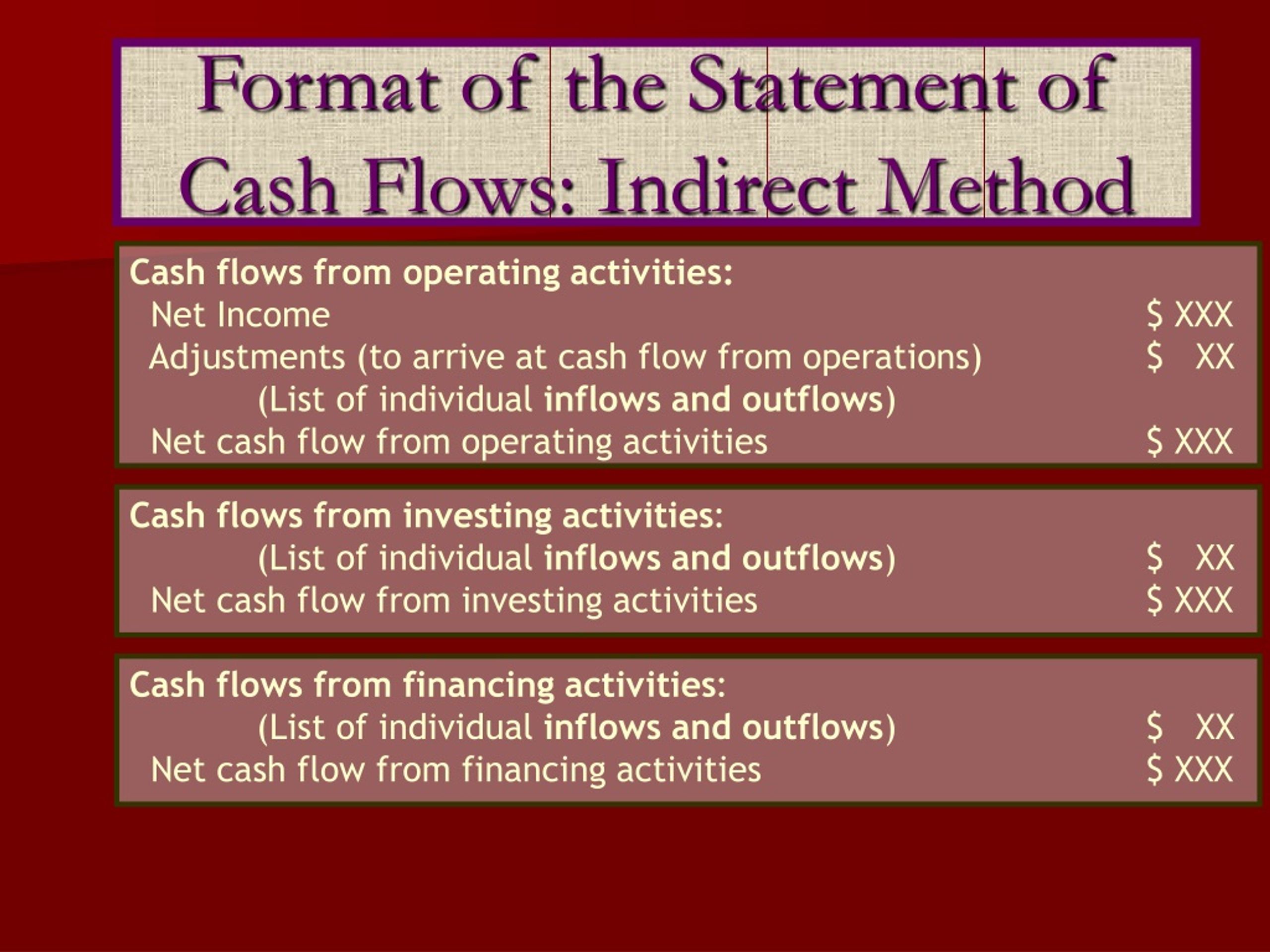

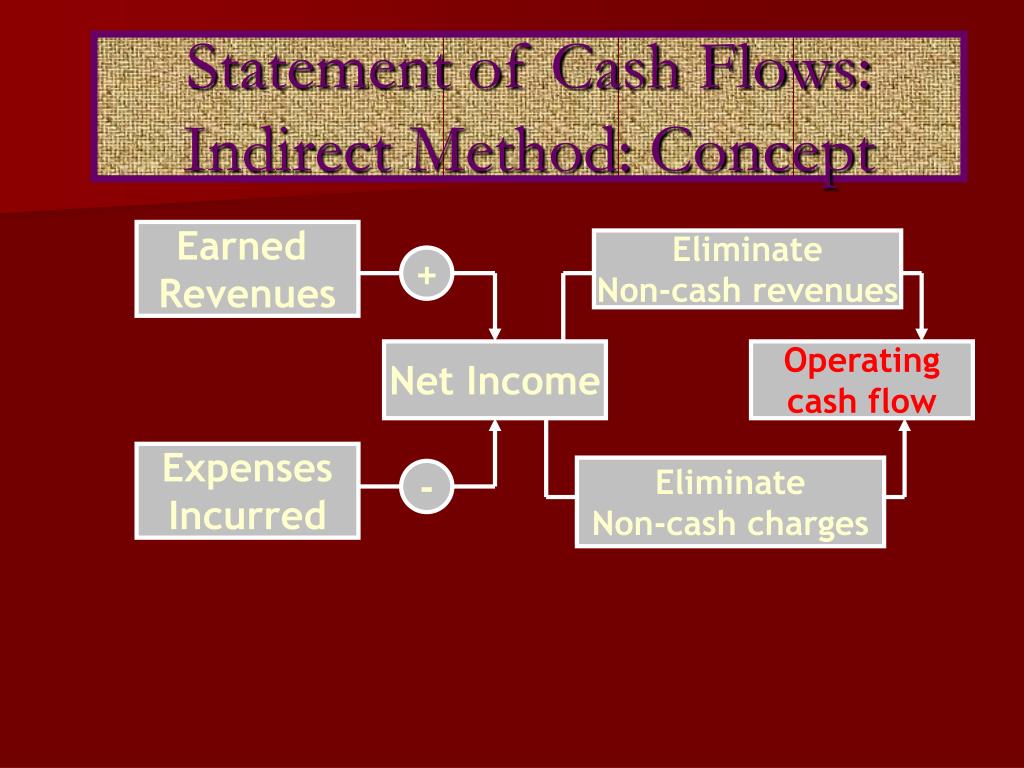

Direct method. reports components of CFs from OA as gross receipts and gross payments. Direct method. requires reconciliation of net income to CF from OA. Direct method. FASB preferred method; however, it is not commonly used. Indirect method. adjusts accrual basis net income to cash basis cash flows from operating activities.

Ch 23 statement of cash flows self study questions by VirginiaBurton4834 Issuu

Statement of Retained Earnings. Step 1 in preparing SCF. Determine change in cash (beginning to end) Step 2 in preparing SCF. Determine cash flows from operating activities. If net income is calculated using accrual basis. difference between net income and cash flows from operations often involves non cash revenues and expenses. Step 3 in.

PPT Chapter 23 Statement of Cash Flows PowerPoint Presentation, free download ID227198

CHAPTER 23 Statement of Cash Flows LEARNING OBJECTIVES After studying this chapter, you should be able to: Describe the purpose of the statement of cash flows. Identify the major classifications.. - Selection from Intermediate Accounting, 15th Edition [Book]

Solution to Chapter 23 Statement of Cash Flow Copyright © 2011 John Wiley & Sons, Inc. Kieso

Study with Quizlet and memorize flashcards containing terms like 21. It is an objective of the statement of cash flows to a. disclose changes during the period in all asset and all equity accounts. b. disclose the change in working capital during the period. c. provide information about the operating, investing, and financing activities of an entity during a period. d. none of these, 22. The.

PPT Chapter 23 Statement of Cash Flows PowerPoint Presentation, free download ID9244480

This information is disclosed on the statement of cash flows (SCF). This chapter discusses the purpose of the statement of cash flows, the steps in preparing the SCF, as well as how to interpret various sections of the statement of cash flows. 11.1: Financial Statement Reporting. 11.2: Preparing the Statement of Cash Flows.

:max_bytes(150000):strip_icc()/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Awesome The Statement Of Cash Flows Classifies Receipts And Payments Basic Balance Sheet Format

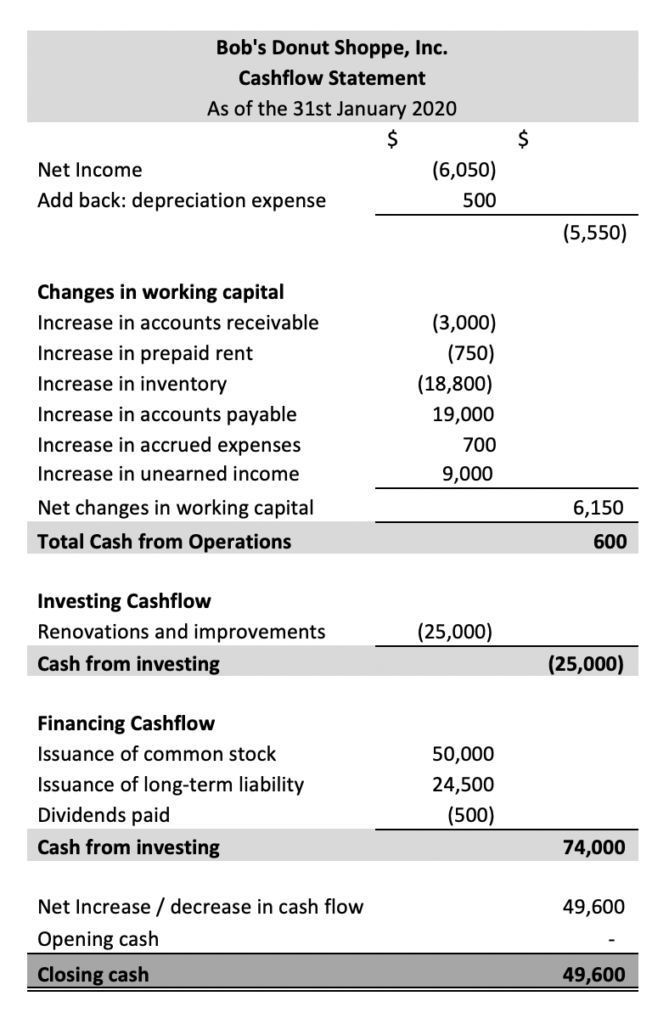

Chapter 23: Statement of Cash Flows 23 - 13 _____ _____ (L. 2) Cashman Company reported net income after taxes of $85,000 for the year ended 12/31/20. Included in the computation of net income were: depreciation expense, $15,000; amortization of a patent, $8,000; income from an investment in common stock of Linda Inc., accounted for under the.

PPT Chapter 23 Statement of Cash Flows PowerPoint Presentation, free download ID227198

1. The entity's ability to generate future cash flows. Primary objective of financial reporting is to provide information with which to predict the amounts, timing, and uncertainty of future cash flows. Helps to better predict the future cash flows than is possible using accrual-basis data alone 2. The entity's ability to pay dividends and meet.

Chapter 23 Statement OF CASH Flows CHAPTER 23 STATEMENT OF CASH FLOWS IFRS questions are

Accounting Standards Codification (ASC) 230, Statement of Cash Flows, addresses the presentation of the statement of cash flows. This publication is designed to assist professionals in understanding the statement of cash flows. This publication reflects our current understanding of this guidance based on our

Understanding Statement of Cash Flows myMusing

A method of preparing a statement of cash flows in which net income is adjusted for items that do not affect cash, to determine net cash provided by operating activities. Study with Quizlet and memorize flashcards containing terms like holdings less than 20%, holdings between 20% and 50%, holdings more than 50% and more.

23 Chapter Statement of Cash Flows Intermediate Accounting

Chapter 23 solution for Intermediate Accounting by Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield (16E) chapter 23 statement of cash flows assignment Skip to document University

What Is a Cash Flow Statement And How Does It Work?

17.2: Direct and Indirect Methods for Preparing a Statement of Cash Flows; 17.3: Cash Flows From Investing and Financing; 17.4: Preparing a Statement of Cash Flow; 17.5: Accounting in the Headlines; 17.6: Exercises- Unit 17;. Chapter License CC BY OER program or Publisher Lumen Show TOC no;

The cash flow statement and it’s role in accounting

This playlist cover cash flow statement, statement of cash flow, converting from cash to accrual, converting from accrual to cash, direct method for operatin.